Stablecoins and the Collapse of the Legacy Payment Model

Why Stablecoins will Unlock the First Trillion Dollar Fintech

Stablecoins aren’t just an improvement on or connective tissue for existing payment rails, they allow companies to bypass those legacy rails entirely and collapse the current payments value chain in on itself. Because if you’re stablecoin native, everything is just a book transfer. A new class of companies are being born (or are adapting) today that understand this — and they will drive the re-architecting of how money moves.

I lead with that because there have been a number of great pieces recently (see Simon Taylor’s posts here and here) about how stablecoins act as a platform, a new banking-as-a-service stack that connects existing rails — from issuer banks through merchant acceptance and everything in between. While I agree, as I think about the future and how companies and protocols can create and accrue value in this new paradigm, I believe the framing of stablecoins as a platform for existing payment rails undersells the true opportunity. This isn’t just a step function improvement like the first wave of APMs (no disrespect to awesome companies like Wise), stablecoins represent the potential to re-imagine how payment rails should be built from first principles.

But to understand where we’re headed, it helps to know how we got here because the context of history reveals the obvious (to me, anyways) evolution.

The Building of our Modern Payment Rails

You can, arguably, trace the beginning of modern payments back to one day in early 1950, when Frank McNamara and his co-founders started Diners Club, the first multipurpose charge card that introduced a closed-loop credit model where Diners Club became the intermediary between a broad set of merchants and cardholders. Prior to Diners Club, almost all payments were either paid in cash or facilitated through localized, proprietary and mainly bi-lateral credit agreements directly between individual merchants and their customers.

Building on the success of Diners Club, Bank of America (“BofA”), seeing the immense opportunity to expand its credit offerings and reach a broader customer base, launched the first mass-market consumer credit card — mailing over 2mm UNSOLICITED, pre-approved revolving line credit cards to primarily middle class consumers who could use them at over 20k merchants across California. Due to regulation at the time, BofA then began licensing their technology to other banks (vs expanding themselves) across the United States and even internationally, creating the first network of issuing banks. The operational challenges were immense, causing disarray and creating massive credit risk that saw delinquency rates soar to above 20% while inviting rampant fraud, almost bringing down the program altogether.

That brings us to a realization by Dee Hock and others that the challenges and disarray within the BofA program and its network of banks could be solved if, and only if, a true cooperative was formed that would manage the system’s rules and infrastructure, allowing members to compete on product and pricing but not on the core infrastructure and standards (sounds familiar, doesn’t it). That cooperative became what we today know as Visa and a similar cooperative, which had been started by a group of California banks that were competing with the BofA program, became Mastercard. This was the birth of our modern “open-loop” four-party payment model that has become the dominant structure for the global payments industry.

From the 1960s and until the early 2000s almost all innovation in payments was about enhancing, supplementing and digitizing that four-party model. And with the booming popularity of the internet, starting in the 1990s, much of that innovation moved to the software stack.

On the back of the internet, e-commerce was essentially invented in the early 1990s — with the first ever web-based secure credit card purchase occurring for a Sting CD on NetMarket, an early online marketplace. That was soon followed by the likes of Pizza Hut’s PizzaNet, the first instance of a national retailer accepting online payments (Pizza is apparently at the cornerstone of all digital innovation). Amazon, Ebay, Rakuten, Alibaba, and other well-known e-commerce startups all launched in the few years after that, leading to the start of many of the first independent payment gateways and processors (tech the merchant needs to accept a payment). Most notably, Confinity and X.com, which merged to become what we now know as PayPal, were both founded in late 1998 and early 1999, respectively.

This was the start of the digital evolution of payments, which has spawned household names with hundreds of billions in equity value that primarily support that traditional payment model. These companies bridge the offline and online worlds and include payment service providers (“PSPs”) and PayFacs like Stripe, Adyen, Checkout.com, Square, and many others. They were launched primarily to solve merchant side problems, by bundling gateways, processing, reconciliation, fraud/compliance tools, merchant accounts, and other value-added software and services — but they did very little to bring the banks and the networks into the internet era.

While there are start-ups focused on disrupting the bank payments and issuing stack, most notable start-ups like Marqeta, Galileo, Lithic, and Synapse have been focused on bringing new companies into existing bank or network infrastructure vs. modernizing, disrupting or improving upon the existing stack. And famously, many of those have found that simply adding a software layer on top of an outdated infrastructure does not, by itself, allow for a true leap forward.

Some entrepreneurs understood those limitations, had the foresight to see that the future needed internet native money and that you could build something better that was not fully dependent on outdated bank infrastructure. Starting most famously with Paypal, many start-ups in the early 2000s were launched with a focus on digital wallets, peer-to-peer transactions, and alternative payment networks that may bypass both or one of the banks and card networks altogether and allow for some monetary sovereignty by the end customer. Those companies include names like Paypal, Alipay, M-Pesa, Venmo, Wise, Airwallex, Affirm, and Klarna.

They often started with a focus on customers who weren’t well served by legacy payment companies and banks — offering a better user experience, a more robust product set, and cheaper transactions, which have resulted in them increasingly taking market share. The banks and networks have clearly felt under attack by these APMs, as Visa and Mastercard launched their own versions called Visa Direct and Mastercard Send, respectively, and banks have launched (sometimes with the government) their own real-time payment networks with a focus on account-to-account transactions. However, while these models have been a step change improvement for many customers, they still suffer from the technical limitations of existing infrastructure. The companies still have to pre-fund and/or take FX/credit risk while netting their own pools of capital against each other vs. being able to actually settle instantaneously and transparently (you might see where this is going).

Essentially, the evolution of modern payments has been closed-loop with trusted intermediaries -> open-loop with trusted intermediaries -> open-loop with partial individual sovereignty. Yet opacity and complexity still reign, leading to a worse user experience and rent extraction across all layers of the stack.

The Evolution of Merchant Payments

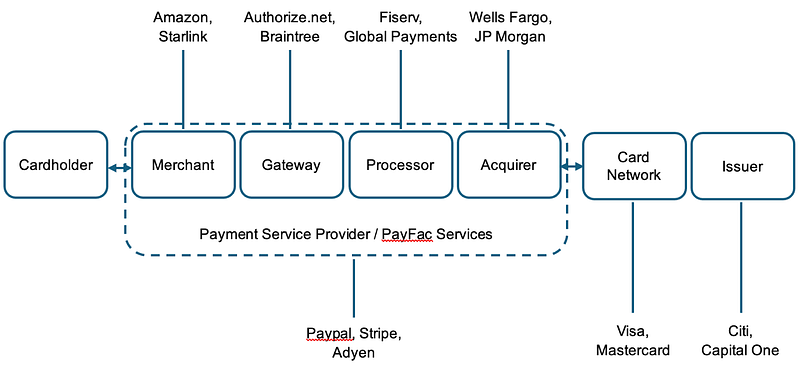

That brings us to today and to the reason stablecoins aren’t just a platform to connect and improve upon those existing providers — but instead are the technical infrastructure companies can build on to bypass parts or all of the legacy stack. Consider the simplified diagram below of the typical merchant payment utilizing a card — and consider @Stripe’s recent moves while looking at it:

And what each of these parts of the stack are responsible for:

Today, Stripe is already handling a significant part of the merchant side of a payment, including even providing the merchant account (being the bank!) and the various pieces of software to run their business and accept payments. But what they don’t do is provide their own card network/scheme or issue cards (yes, I know they have a BaaS card issuing program that utilizes a third-party issuing bank underneath).

Now, imagine a world where Stripe, through@stablecoin""> @stablecoin and utilizing stablecoins, is actually the central bank, issuing their own stablecoin (backed by approved collateral per the GENIUS act) that can atomically settle across consumer (cardholder) and merchant accounts (wallets like@privy_io""> @privy_io) utilizing a transparent and open-source ledger (blockchain). You don’t need both an issuing and merchant bank, Stripe (or any other issuer) just needs a single bank(s) who can hold the collateral for their issued stablecoin. You don’t need the card network to route the information to appropriate counterparties — they transacted directly from their wallets on a blockchain — or, if needed, via a request to mint/redeem at Stripe (the issuer/central bank), who then settles to a blockchain. You also don’t need the network to facilitate the clearing and settlement of funds, as that can happen either atomically or utilizing a series of smart contracts that can provide structures to handle charge backs and disputes (see Circle refund protocol). Similarly, routing of payouts or even swaps into other currencies/products can be done programmatically. Standardization of data passing from banks to gateways, processors, and networks is significantly easier because you no longer have a Frankenstein tech stack piecing together both legacy and modern systems (see@coinbase""> @coinbase x402). And both fees and reconciliation are easier due to the transparent nature of the data and reduction in stakeholders.

In that world, all of a sudden, it starts to look like Stripe (and other start-ups working on this) have collapsed much of the current payment model in on itself — owning the full stack to offer accounts, issuing, credit, payment services, and network all enabled by existing on a better tech rail that has fewer intermediaries and gives almost full control of money movement to the holder of the wallet.

As Simon Taylor said to me when they graciously read the first draft of this post, “Everything is a book transfer if you’re stablecoin native. The merchant, gateway, PSP, and acquiring bank all had to reconcile different ledger entries. With stablecoins all of that is pushed externally, so anyone operating with stables is the gateway, PSP and acquiring bank in one, and everything is a book transfer.”

Does that world look like a sci-fi novel based on what we have today? Absolutely. Are there a significant number of potential problems I glossed over related to fraud, compliance, usability of stables vs. offramping, liquidity/costs, etc? You bet ya. Will there be incremental steps between where we are today and this potential future, if we ever get it? No doubt in my mind. Will things like RTPs make this less attractive? Maybe, but programmability and interoperability across FX/the treasury stack is something an RTP can’t solve.

Regardless, this future is coming and it’s clear that some are preparing themselves for this likelihood. Look no further than how other top issuers like@Circle""> @Circle (see CPN),@Paxos""> @Paxos, and@withausd""> @withausd are evolving their product set or how payments focused blockchains (@Codex_pbc"">@Codex_pbc,@Sphere""> @Sphere,@PlasmaFDN""> @PlasmaFDN) are moving up stack to the end consumer/business. And in this future the network has, at worst, less intermediaries, more self sovereignty, more transparency, better value capture by the customer, and more interoperability.

Cross Border Payments (this one is obvious, right?)

Let’s now consider what the B2B payments flow looks like for cross-border as it’s one of the areas where we have seen a significant amount of uptick for stables so far (see the data from Artemis in a report we and Castle Island co-authored with them).

Matt Brown had an excellent explainer post on this late last year — from that post:

While simplified, this correctly outlines that in many cases there will be multiple banks that exist in the middle of a cross border transaction, all utilizing swift messaging (not bad by itself, but the back and forth between banks is), often with other clearing counterparties involved. In fact, it’s not uncommon for this process to take 7–14 days to clear, creating significant risk and cost. The flow is extremely opaque, sometimes requiring a customer to call the originating bank directly just to get an update — and even then, they may still be in the dark. In fact, one start-up founder that came from a large corporation told me that it was not uncommon for JP Morgan to “lose” millions for weeks while transferring treasury funds from a U.S. parent company to a foreign subsidiary. On top of that, there is FX risk involved across multiple counterparties causing the average transaction to cost 6.6%. And the ability to access USD and yield bearing accounts for those engaged in cross border money movement is extremely low for all but the largest of enterprises.

So it may come as no surprise that we also saw Stripe recently announce stablecoin powered financial accounts. This allows businesses access to a US dollar financial (e.g. bank) account backed by stablecoins, to mint/redeem stablecoins directly from Bridge, to move money globally through the Stripe dashboard to other wallet addresses, on-ramp and off-ramp using bridge APIs, issue a card (depending on location and today utilizing Lead Bank) backed by your stablecoin balance, swap into other currencies, and eventually swap directly into yield bearing products for treasury management. While much of this is still dependent on the traditional system as a stop gap solution, the sending/receiving/issuing/swapping of stablecoins and tokenized assets is not. The first solution where there is a need for on-ramping/off-ramping fiat is much like the current state of APMs — companies like Wise and Airwallex, who have done a tremendous job of essentially creating their own bank network and parking capital in different countries and currencies while netting at the end of the day. Jack Zhang, the co-founder of Airwallex, correctly pointed this out last week, but he didn’t consider how the world would change if off ramping is no longer needed.

If you can stay in those tokenized assets (likely requiring local stables), utilize them, and not have to swap to fiat then you’ve essentially bypassed the traditional correspondent bank model altogether. That creates a world where the reliance on a third party for the actual holding and sending of assets goes (mostly) away -> allowing the customer to capture significantly more value and lowering cost for everyone. Start-up companies like@Squadsprotocol""> @Squadsprotocol (accounts),@Raincards""> @Raincards (cards),@Stablesea_xyz""> @Stablesea_xyz (fx/treasury mgmt) and many others are all working on parts of the stack to make staying in tokenized assets more of a reality — and, while they haven’t told me this is their plan, I expect all companies operating here to eventually move across the stack. Again, collapsing the value chain because you can — because all money movement in stablecoins is just a book transfer.

But even if you want to utilize fiat, companies like@ConduitPay""> @ConduitPay work directly with the largest FX banks in the local markets to make seamless, cheap, and near instant cross border transactions happen on chain and with stablecoins. Again, the wallets become the account, the tokenized assets become the products, the blockchain is the network, and you’ve now got a significantly better user experience that without the need for off ramping CAN be cheaper. All done with better tech that offers easier reconciliation, more sovereignty, greater transparency, faster speed, improved interoperability and even (potentially) lower cost.

So What Does All this Mean (don’t worry, I’m wrapping up)?

It means that a world where payments exist onchain, natively utilizing stablecoins (a book transfer), is coming — it’s not just going to connect the current payment model, it’s going to collapse it. And that’s why we will see the first trillion dollar fintech built on stablecoin rails, because the value chain no longer needs to bifurcate.

While I know there will be a lot of valid criticisms to this post about how I didn’t consider xyz issue, understand that I and many of the entrepreneurs building in this space realize that and are working to solve those issues. That’s how innovation has to work — because building for another incremental change never, actually, brings real, net new systems. Especially in a market where the entrenched incumbents will lobby against a future that makes them less relevant before, eventually, launching half measures in hopes of participating. And when that happens, you will know what is coming next.

closed-loop with trusted intermediaries -> open-loop with trusted intermediaries -> open-loop with partial individual sovereignty -> truly open digitally native systems where everyone can compete across the entire stack and customers exercise self sovereignty utilizing open networks

This publication represents the subjective views of the author and are not necessarily the views of Dragonfly or its affiliates. Funds managed by Dragonfly may have invested in some of the protocols and/or cryptocurrencies mentioned herein. This publication is for general information and discussion purposes and is not general or personal investment advice, it does not contain all material information pertinent to an investment decision and should not be used as the basis for any investment or relied upon in evaluating the merits of any investment. Statements contained in this publication are based on current expectations, estimates, projections, opinions, and beliefs. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon.

Disclaimer:

- This article is reprinted from [HadickM]. All copyrights belong to the original author [HadickM]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Related Articles

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

What is Stablecoin?

Top 15 Stablecoins

A Complete Overview of Stablecoin Yield Strategies

What Is USDT0